Serial Differencing Aggregation

editSerial Differencing Aggregation

editSerial differencing is a technique where values in a time series are subtracted from itself at different time lags or periods. For example, the datapoint f(x) = f(xt) - f(xt-n), where n is the period being used.

A period of 1 is equivalent to a derivative with no time normalization: it is simply the change from one point to the next. Single periods are useful for removing constant, linear trends.

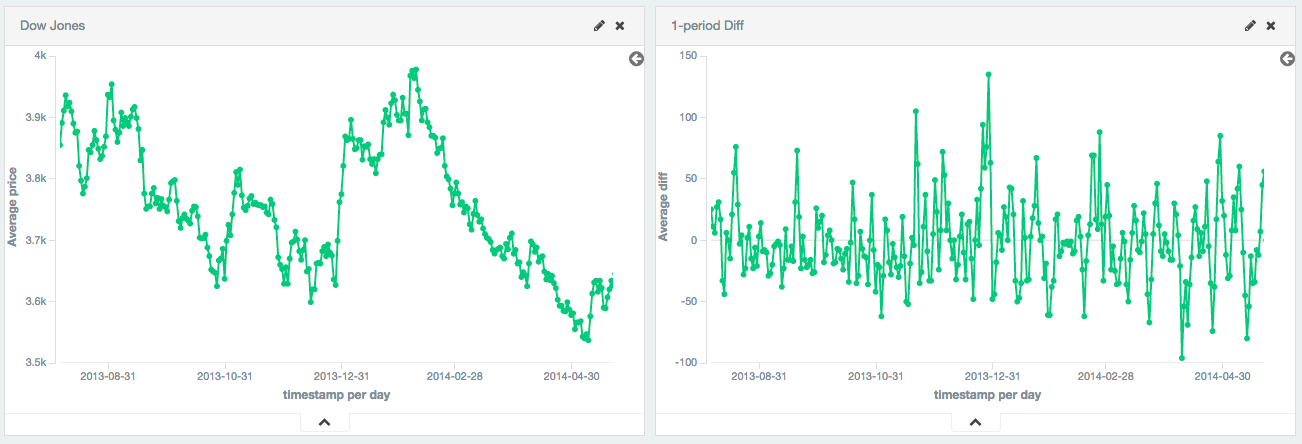

Single periods are also useful for transforming data into a stationary series. In this example, the Dow Jones is plotted over ~250 days. The raw data is not stationary, which would make it difficult to use with some techniques.

By calculating the first-difference, we de-trend the data (e.g. remove a constant, linear trend). We can see that the data becomes a stationary series (e.g. the first difference is randomly distributed around zero, and doesn’t seem to exhibit any pattern/behavior). The transformation reveals that the dataset is following a random-walk; the value is the previous value +/- a random amount. This insight allows selection of further tools for analysis.

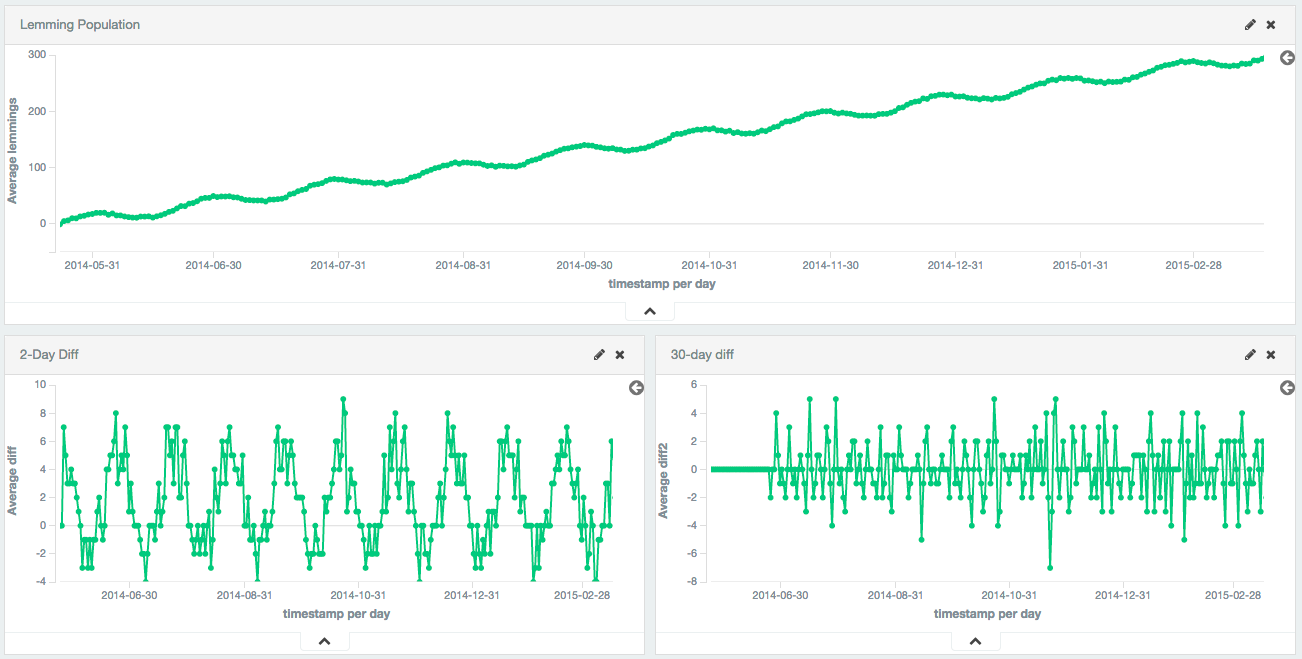

Larger periods can be used to remove seasonal / cyclic behavior. In this example, a population of lemmings was synthetically generated with a sine wave + constant linear trend + random noise. The sine wave has a period of 30 days.

The first-difference removes the constant trend, leaving just a sine wave. The 30th-difference is then applied to the first-difference to remove the cyclic behavior, leaving a stationary series which is amenable to other analysis.

Syntax

editA serial_diff aggregation looks like this in isolation:

{

"serial_diff": {

"buckets_path": "the_sum",

"lag": "7"

}

}

Table 30. serial_diff Parameters

| Parameter Name | Description | Required | Default Value |

|---|---|---|---|

|

Path to the metric of interest (see |

Required |

|

|

The historical bucket to subtract from the current value. E.g. a lag of 7 will subtract the current value from the value 7 buckets ago. Must be a positive, non-zero integer |

Optional |

|

|

Determines what should happen when a gap in the data is encountered. |

Optional |

|

|

Format to apply to the output value of this aggregation |

Optional |

|

serial_diff aggregations must be embedded inside of a histogram or date_histogram aggregation:

POST /_search

{

"size": 0,

"aggs": {

"my_date_histo": {

"date_histogram": {

"field": "timestamp",

"calendar_interval": "day"

},

"aggs": {

"the_sum": {

"sum": {

"field": "lemmings"

}

},

"thirtieth_difference": {

"serial_diff": {

"buckets_path": "the_sum",

"lag" : 30

}

}

}

}

}

}

|

A |

|

|

A |

|

|

Finally, we specify a |

Serial differences are built by first specifying a histogram or date_histogram over a field. You can then optionally

add normal metrics, such as a sum, inside of that histogram. Finally, the serial_diff is embedded inside the histogram.

The buckets_path parameter is then used to "point" at one of the sibling metrics inside of the histogram (see

buckets_path Syntax for a description of the syntax for buckets_path.